Definition

The GRI is an international independent standards organization and currently issues one of the most well-known standards for ESG reporting (GRI Standards).

Some other commonly used ESG standards are the ISO 26000, SASB, and CDP.

ESG reporting standards are a specific category of guidance that provides specific, replicable, and detailed information on best practices for disclosing sustainability information.

Standards are key for sustainability reporting because they provide metrics and regularity to the field, thus creating a common blueprint for making frameworks actionable.

Companies will typically announce the standard that they are using for their reports, but there is currently no universal external verification for whether the standard has been applied well.

Note that the GRI does have a Report Registration System, but this system does not check report content; it only scans for the correct claim language and whether the information through the system process is correctly aligned with the registered report.

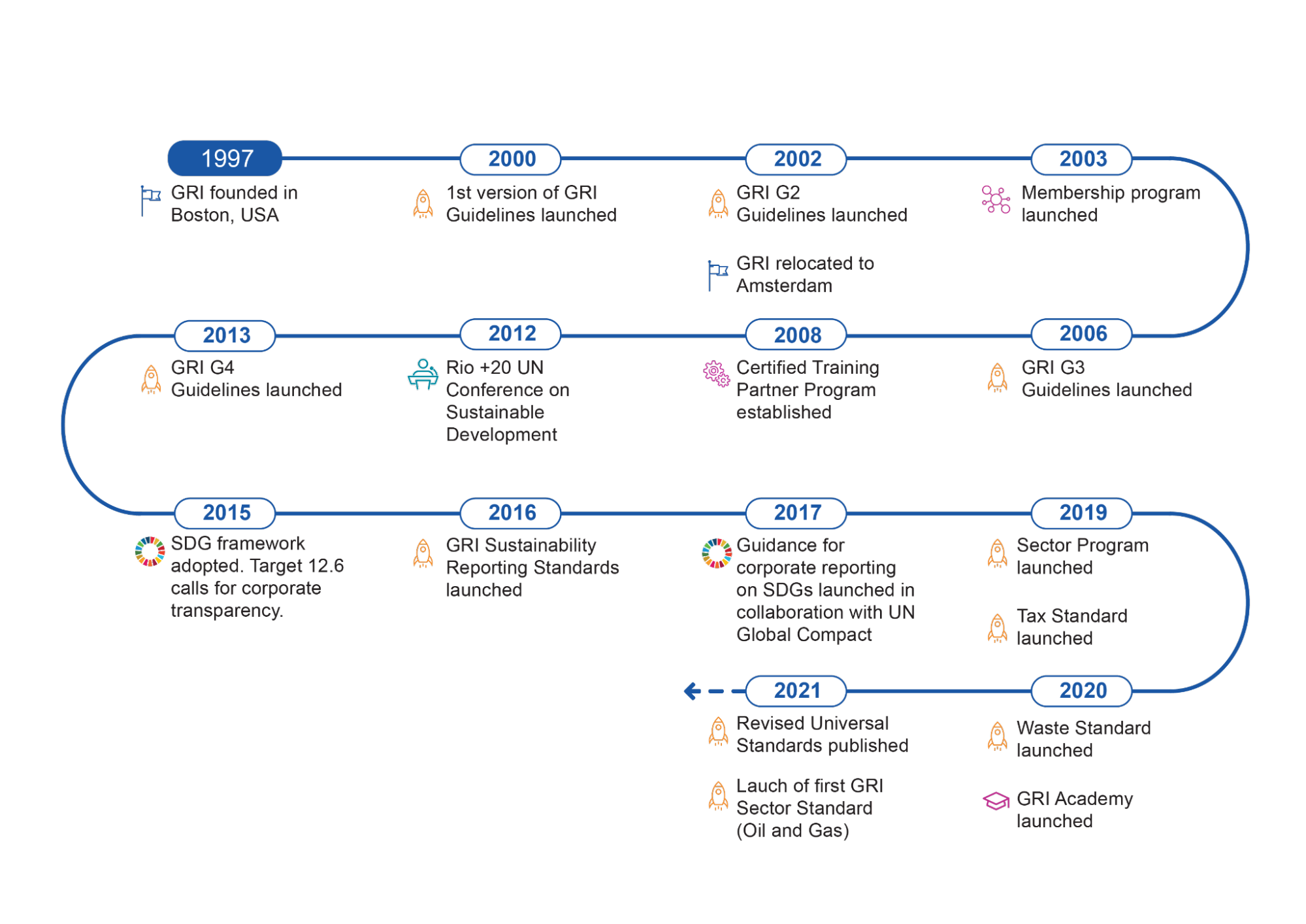

History of the GRI and GRI Standards

The GRI was created in 1997 by two non-profits, Ceres and the Tellus Institute, along with the support of the United Nations Environment Programme (UNEP).

The aim of the GRI as a standard setting organization is to enable companies or third parties to assess environmental impact in a cohesive, rigorous way that is widely accepted by others.

The GRI Standards were the first globally accepted standard for sustainability reporting, and are set by the Global Sustainability Standards Board (GSSB), an independent operating entity comprised of 15 members.

Some key dates for the establishment and growth of the GRI Standard include:

- 1997: Founded following the Exxon Valdez oil spill

- 2000: Released first full draft of the Sustainability Reporting Guidelines

- 2008: GRI establishes their Certified Training Partner Program

- 2016: The GRI Standards launched

- 2019-2021: GRI launches the Sector Program, Tax Standard, Waste Standard, GRI Sector Standard, and the Revised Universal Standards

GRI Standards today

Response to demands for clarity in sustainability reporting

In September of 2020, the GRI joined with the SASB, CDP, CDSB, and IIRC to develop a single set of comprehensive and global reporting standards.

The GRI and SASB also started a joint project in the same year, focusing on communication materials to help stakeholders better understand how to use GRI Standards and SASB Standards concurrently.

They have since published A Practical Guide to Sustainability Reporting Using GRI and SASB Standards in April 2021.

GRI Standards growth trends

Overall, the GRI Standards are still the most widely used sustainability reporting standard.

The 2020 KPMG Survey of Sustainability Reporting found that across the world’s largest 250 companies (the G250), the GRI Standards is the only sustainability reporting standard with widespread global adoption.

They also report that as of 2020, 73% of the G250 and 67% of the N100 use the GRI Standards.

However, given the trend towards consolidation and collaboration between the leading sustainability reporting standards, in the future we will most likely see standards being used in synergy, rather than in competition.

Limits and Controversy

Since its introduction, the GRI Standards have been extremely influential.

However, as with all sustainability standards, it faces the challenge of creating a universally applicable Standard while keeping the reporting process straightforward.

Some barriers to the widespread adoption of the GRI Standards, as identified by a researcher from the University of Waterloo, include the general lack of cohesiveness among the different sustainability standards and the necessary interdependence among elements of the GRI Standards (meaning that using the GRI Standards only partially may not be that useful).

The GRI is limited in that it is a topic level reporting framework, meaning that despite the modular nature of the GRI Standards, GRI guidance is still less specific than other reporting frameworks such as the SASB.

The SASB provides instruction on things like disclosure topics and accounting/activity metrics on a granular level, while the GRI has a broader but shallower scope.

Controversy around the GRI mainly centers on whether it accomplishes its goal of providing a single standard for sustainability reporting, and people have different opinions in this regard, with the overwhelming majority supporting it as a respected universal standard.

Related articles

Global Reporting Initiative: What It Is and How to Do It

GRI stands for Global Reporting Initiative, and is an international independent standards organization that promotes sustainability reporting through the development of global standards for corporate responsibility, including environmental, social and governance (ESG) reporting...

Corporate Sustainability Reporting Directive: All you need to know

The Corporate Sustainability Reporting Directive is an EU regulation that will have a huge impact on how organisations report their environmental, social and governance (ESG) performance...

Discover the latest Sustainability Recent Developments to improve your companies

Sustainability is a concept that evolves due to pressing sustainability challenges, worldwide issues, and its own concept limits. New concepts have emerged to think further and respond better to all the world’s current challenges...

What is Materiality and Why it matters in business

Materiality is crucial for sustainability reporting because it allows companies to focus on the most important aspects of their sustainability efforts. A company can choose to report on all aspects of its sustainability program, but this would be extremely time-consuming and would probably not be very useful for investors and other stakeholders...

The concept of impact on social and environmental issues and its implication for companies

Impact measurement is a powerful tool for companies to gauge their impact on social and environmental issues. In this article, we will discuss the concept of impact, its implications for organizations, and how it can be measured...

The most important and recent developments of ESG (Environmental, Social and Governance)

Being a B Corporation is not just about making profits and creating wealth for a company, it is a way of creating a more sustainable future for society! Discover our article about B corps and its benefits here...

The process for an enterprise to get the B corp certification

Becoming a B Corporation is an ambitious undertaking. This article will guide you through the steps required to become a B Corporation…

What is a B Corporation: what this means and its benefits for companies

Being a B Corporation is not just about making profits and creating wealth for a company, it is a way of creating a more sustainable future for society! Discover our article about B corps and its benefits here...

The guide to EcoVadis certification: frequently asked questions

This guide will take you through the steps of the EcoVadis Certification process, and explain what is involved in becoming a certified business...

The implications of ISO 26000 for companies

ISO 26000 is a standard providing direction for the application of social responsibility to the activities of an organization. But what does this mean? And how can organizations use it to create better and more sustainable business practices? Let's talk about it…

What is the meaning of CSR (Corporate social responsibility) and how to adopt it?

A Corporate Social Responsibility strategy refers to an organization's active consideration of the effects its activities have on the environment, employees, customers, and suppliers. Let's look at how your company could adopt such a program...

4 reasons companies should adopt CSR, Corporate social responsibility

CSR is all about managing a company’s externalities while creating sustainable value for stakeholders and continuous innovation for the business. Let's break that down and explore why...

Carbon disclosure project reporting: what is it and how does it work?

Read our article about The Carbon Disclosure Project (CDP), an extra-financial questionnaire that collects data on companies’ environmental practices and performance...

What are the differences between Corporate Social Responsibility (CSR) and Environmental Social Governance (ESG)?

These terms are both used to describe an approach for businesses to integrate social and environmental factors into their governance policies, strategies, processes, and programs. Yet, they're not the same. Let's explore their key differences...

Why is ESG (Environmental, Social and Governance) important for a business

ESG (environmental, social and governance) can help businesses make sound decisions, and investors achieve better long-term returns. Let's discover how...