The Corporate Sustainability Reporting Directive is a European Union law that will have a huge impact on how organisations report their environmental, social and governance (ESG) performance.

The CSRD was introduced on January 1, 2020, and will affect organisations that have a listing on a regulated market in the European Union or that reach certain thresholds (number of employees, turnover, balance sheet).

The new directive will require organisations to publish more information about their environmental impact, social and economic performance, as well as governance practices.

The reports must also include information about the risks and opportunities associated with these areas.

In this article we explain what the directive is, who it affects and the steps you can take to prepare for its enforcement.

Background

In order to achieve the EU’s goal of becoming net-zero by 2050, the European Commission recognizes that private capital must be directed toward green, sustainable projects.

To accomplish this, the Commission believes that investors must have direct exposure to complete and coherent information on their potential investees, including information on environmental practices, social responsibility and governance mechanisms.

The Corporate Sustainability Reporting Directive (CSRD) represents one key legislation piece that will facilitate the transition towards a more sustainable society, aiming to fill in the gaps in sustainability reporting.

It completes two other regulations which go in the same direction: the Sustainable Finance Disclosure Regulation (SFDR) and the EU Taxonomy.

Overall, the CSRD will supersede and complement the Non-Financial Reporting Directive (NFRD). Directive 2014/95/EU Directive 2014/95/EU, which is referred to as the Non-Financial Reporting Directive (NFRD), sets forth the regulations on disclosure of non-financial and diversity data by certain major firms.

NFRD came into force in all EU member states in 2018. All 27 nations had subsequently adopted the Directive into national legislation, and it is now up to corporations to comply.

It compels some major corporations to provide a non-financial statement as part of their yearly public reporting responsibilities.

With the NFRD, the European Union aimed to accomplish two major goals: make non-financial information about a company’s value creation as well as its risks available to stakeholders and investors, and effort to improve to assume accountability for social and environmental concerns.

From NFRD to CSRD

The Non-Financial Reporting Directive’s reporting requirements set critical criteria for some major corporations to report on their sustainability performance on an annual basis.

It established a double materiality viewpoint,’ which requires businesses to report on the effect of sustainability challenges on their operations as well as their own impact on people and the environment.

Nonetheless, abundant evidence was shared that the data provided by businesses is insufficient. Investors and other stakeholders often believe that reports exclude critical information.

Comparing reported data from one organisation to another may be difficult, and users of the data are sometimes uncertain about its reliability. Quality issues in sustainability reporting have a cascading impact.

As a result, investors lack a comprehensive perspective of the sustainability risks exposed to businesses.

Investors are becoming more interested in the social and environmental effect of businesses.

They need this knowledge in part to comply with the Sustainable Finance Disclosure Regulation’s own disclosure obligations.

More broadly, investors must understand the sustainability effect of the firms in which they participate if the market for green investments is to be viable.

Without such information, funding for ecologically beneficial initiatives cannot be directed.

Finally, deficiencies in reporting quality create an accountability chasm.

Companies that provide high-quality and dependable public reporting will contribute to the development of a more effective disclosure ecosystem.

CSRD precisely aims to dramatically broaden the scope of the NFRD while also increasing the transparency of business progress in terms of long-term sustainability and environmental protection.

The full requirements of the reporting duties under the CSRD will be specified in the new sustainability reporting standards that are currently being finalised under the supervision of the European Financial Reporting Advisory Group (EFRAG), which is a private organisation founded in 2001 at the European Commission’s request to serve the public interest.

CSRD, SFDR and the EU Taxonomy

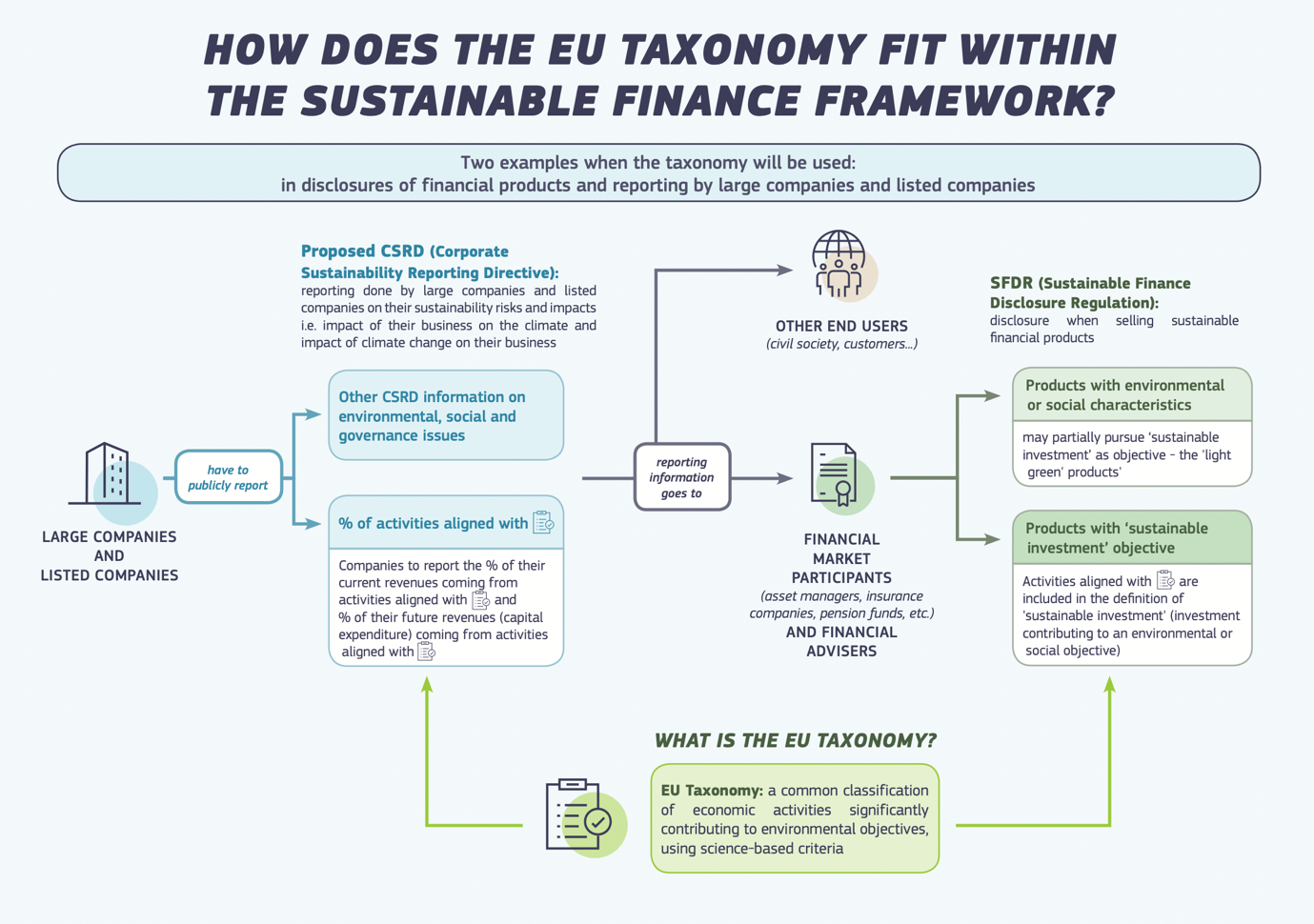

The CSRD may be seen as one of three EU rules governing sustainability reporting, alongside SFDR and the EU Taxonomy. The Sustainable Finance Disclosure Regulation (SFDR) came into force in March 2021.

By standardising sustainability disclosures, the SFDR aims to assist institutional investors and clients in understanding, comparing, and monitoring the sustainability features of investment funds.

The EU Taxonomy Regulation was published in the European Union’s Official Journal on 22 June 2020 and adopted on 12 July 2020.

It lays the groundwork for the EU Taxonomy by outlining four broad criteria that an economic activity must fulfil in order to be considered environmentally sustainable.

Whereas the Sustainable Finance Disclosure Regulation (SFDR) is intended to steer investments into sustainable economic activity, the EU Taxonomy determines which economic activities are really “sustainable”.

Article 8 of the Taxonomy Regulation compels enterprises covered by the current Non-Financial Reporting Directive – as well as any new companies covered by the CSRD – to report on the sustainability of their operations. Companies will be required to submit these metrics in addition to other sustainability data required by the CSRD.

Hence, these three regulations are inextricably linked: corporations subject to CSRD are required to make Taxonomy-related disclosures; their reporting is routed via financial market participants, who are subject to SFDR reporting obligations that include Taxonomy-related disclosures as well.

As a result, concerned firms may anticipate increased pressure from investors to publish sufficient sustainability information in accordance with the CSRD and the EU Taxonomy.

Intertwining of the 3 key regulations on non-financial reporting in Europe:

Source: European Commission

Objectives

The CSRD aims to build upon the existing objectives of the NFRD.

The following are the aims of the proposal:

- Requiring that reported information be compatible with EU legislation, including the EU Taxonomy, be comparable, trustworthy, and simple for interested parties to access and utilise using digital technologies.

- Eliminating wasteful expenditures and allowing businesses to fulfill the rising demand for sustainability reporting in a cost-effective way.

CSRD: Scope of Application

The CSRD will broaden the scope of sustainability reporting obligations to include all major businesses that do not meet the NFRD’s existing 500-employee criterion.

All significant firms will be held publicly responsible for their effect on people and the environment as a consequence of this evolution. NFRD applies to “large” public interest entities (“PIEs”).

PIEs are classified as those organisations who have had more than 500 workers in the prior financial year.

The NFRD also absolves subsidiaries from reporting responsibilities if that entity’s parent firm agrees to perform the reporting obligations on behalf of the whole group.

Once operational, the CSRD would expand non-financial reporting obligations to big private corporations as well as those listed on EU regulated markets.

Approximately 12,000 businesses are presently subject to the Non-Financial Reporting Directive.

The European Commission predicts that this figure might climb to around 49,000 under the CSRD, owing to the greater definition of “large undertaking” under the Directive, as opposed to the large PIEs under the Non-Financial Reporting Directive.

Companies who fulfill two of the three requirements outlined below will be required to comply with the CSRD:

- Net turnover of more than €40 million.

- Balance sheet assets greater than €20 million

- More than 250 employees

CSRD has been established to encompass all major and publicly traded corporations operating on EU-regulated marketplaces (except for micro-enterprises).

Small and medium-sized enterprises (SMEs) listed on the EU regulated markets have to comply with the CSRD but on an extended schedule.

Additional requirements for CSRD compliance apply to non-EU-based corporations having subsidiaries in the EU and companies that are not formed in the EU but have securities listed on EU-regulated markets.

Practical requirements under CSRD

The following are the most paramount implications brought forward by CSRD:

- broadens the scope to include all major firms and all publicly traded companies on regulated marketplaces (except listed micro-enterprises)

- increases reporting requirements and standardisation of disclosure, including a requirement to report in accordance with mandatory EU sustainability reporting standards that are in the process of being finalised. This will allow comparability of data between disclosing companies

- requires auditing (assurance) of reported information

- requires businesses to digitally 'tag' reported information, making it machine-readable and feeding into the European single access point envisaged in the capital markets union action plan.

Information that should be disclosed by companies

Under CSDR, the Commission currently suggests that obligatory disclosures be included in a company’s management report and address three reporting areas:

1. Strategy

- Business model and strategy

- Primary risks regarding sustainability issues and dependencies

- Management and supervisory bodies' roles in relation to sustainability

2. Implementation

- Due diligence procedures for operations and the supply chain

- Policies addressing sustainability factors

- Sustainability targets

3. Performance

- Indicators pertinent to measuring all of the above

- Progress toward meeting targets

The CSRD covers all ESG criteria: environmental, social and governance issues.

In particular, the European Sustainability Reporting Standards (ESRS) issued in last April address the following 13 ESG topics:

Environment

- Climate change

- Pollution

- Water and marine resources

- Biodiversity and ecosystems

- Circular economy and resource use

Social

- Own workforce

- Workers in the value chain

- Affected communities

- Consumers and end-users

Governance

- Governance, risk management and internal control

- Business conduct

Lastly, three levels of information are expected:

- Mandatory industry-agnostic disclosures, which have been specified by EFRAG in the cross-cutting ESRS mentioned above.

- Mandatory industry-specific disclosures. Companies will have to report on a series of mandatory standards according to their sector of activity. These are currently being defined and will be published in the form of a Delegated Act in June 2024.

- Company-specific information on issues that the company considers important and that have not been covered in the rest of the sustainability report.

Conceptual guidelines CSRD

CSRD provides guidelines on how to take into account certain key concepts:

- Information quality: requirements on how to ensure quality of sustainability data (e.g truthful representation, comparability, verifiability, etc.).

- Double Materiality: determining both the importance of sustainability issues on the company’s performance (i.e. financial materiality) and the external impacts of the company’s activities on the economy, the environment and people (i.e. impact materiality).

- Time horizon: the reporting period for sustainability information should be consistent with the one retained for financial statements, with additional retrospective and forward-looking information.

- Boundaries and value chain: sustainability data should cover direct and indirect business relationships in the upstream and/or downstream value chain

Reporting under CSRD

As part of the CSRD, financial and sustainability information will be released simultaneously within the management report.

A third-party assurance on the reported information will become necessary.

Moreover, companies will have to digitise and identify their sustainability information to make it accessible via the EU’s forthcoming European Single Access Point (ESAP) database.

Important data will need to be “tagged” or given a “digital label” in order for algorithms to read it more quickly and for stakeholders to exploit and evaluate it.

How to prepare for CSRD

Given the breadth and reach of this law, most companies are likely to be seriously affected. Nonetheless, it is important to mention that for companies under NFRD there is no major change yet, until the regulator will release the final EFRAG Standards in late 2022.

For companies newly under CSRD’s scope, there are several steps to take to facilitate this transition. Businesses will want to get acquainted with the proposal itself and the actual implications of its needs for their firm.

The board of directors should ensure that the management team adequately prepares the firm for the new directive’s implementation, commencing immediately with planning.

While the board of directors will oversee the company’s preparations on a broad scale, the audit committee will play a critical role.

It should supervise the establishment of any new measurement and reporting procedures and the efficacy of the systems and controls in place to assist in guaranteeing the robustness of the information provided.

Since the sustainability reporting requirements are still being developed, businesses will need to begin preparations without knowing detailed requirements.

As a result, businesses should stay informed of any EFRAG findings, interpretations, and communications that provide early insight into how the standards will likely appear.

What is certain right now is that companies need to work on their ESG risks / double materiality analysis and then identify existing policies and KPIs covering those risks, and if none, close the gaps by formalising new ones.

Penalties for non-compliance with CSRD

Each Member State will define penalties for infringements to the CSRD.

The EU Commission has specified that sanctions must be “effective, proportionate and dissuasive” in its draft proposal.

This is generally consistent with the present NFRD. However, the CSRD goes further, requiring member states to implement the following (administrative) measures as well:

- a public declaration describing the infraction and identifying the guilty person/entity;

- a cease-and-desist order against the accountable person/entity;

- an administrative pecuniary penalties against the responsible person/entity.

Audit Requirements

The CSRD proposal establishes a common EU-wide audit (assurance) requirement for submitted sustainability data, assisting in ensuring that provided data is accurate and credible.

While the European Commission’s purpose is to achieve a comparable degree of certainty for financial and sustainability reporting, it has allowed for a gradual approach.

Initially, auditors should give an opinion predicated on a “limited assurance” involvement with the sustainability reporting’s compliance with the CSRD’s criteria, including relevant reporting standards.

It is envisaged that the “limited” guarantee will be changed to a “reasonable assurance” at a later date, after the publication of the sustainability criteria and a review by the European Commission within three years of the CSRD taking effect.

Costs of CSRD

Although the EU plan seeks to “lower the superfluous expenses of sustainability reporting for enterprises,” it is projected that preparers would spend considerable one-time fees as well as recurrent yearly costs in order to comply with the regulation.

The suggestion emphasises that corporations are already facing an increasing financial burden as a result of stakeholders demand for sustainability information.

As a consequence, depending on their size, businesses might realise significant savings by implementing the standards, since the standards eliminate the need for further information requests.

Next steps

- October 2022 - The final set of ESRS will be published by the EFRAG.

- January 2024 - Companies subject to the NFRD's non-financial reporting obligation (large listed companies with more than 500 employees) will be required to disclose accordingly to the new CSRD reporting requirements.

- January 2025 - All companies meeting two of the following three criteria will be subject to reporting requirements: 250 employees, €40 million in revenues, or €20 million in balance sheet.

- January 2026 - Listed small and medium-sized enterprises (10-250 employees) may be able to defer their reporting obligation for up to three years with a lighter standard.

- January 2028 - European subsidiaries of non-European companies with a turnover of more than €150 million in Europe will have to comply with new reporting requirements.

In conclusion…

As regulations become more stringent and the business world becomes more socially and environmentally aware, ESG practices will be mandated.

If your company must comply with the CSRD, you should begin immediately. The deadline is coming up fast, and the fines for noncompliance can be steep.

But it can be a time-consuming and complex process.. And that’s where we come in to help!

Apiday provides a platform that simplifies the data collection process of sustainability metrics and unlocks seamless collaboration.

So you can focus on what matters the most: driving change in your company rather than fetching and crunching data!

Get started and book a call with our ESG experts!

Related articles

Global Reporting Initiative: What It Is and How to Do It

GRI stands for Global Reporting Initiative, and is an international independent standards organization that promotes sustainability reporting through the development of global standards for corporate responsibility, including environmental, social and governance (ESG) reporting...

Discover the latest Sustainability Recent Developments to improve your companies

Sustainability is a concept that evolves due to pressing sustainability challenges, worldwide issues, and its own concept limits. New concepts have emerged to think further and respond better to all the world’s current challenges...

What is Materiality and Why it matters in business

Materiality is crucial for sustainability reporting because it allows companies to focus on the most important aspects of their sustainability efforts. A company can choose to report on all aspects of its sustainability program, but this would be extremely time-consuming and would probably not be very useful for investors and other stakeholders...

The concept of impact on social and environmental issues and its implication for companies

Impact measurement is a powerful tool for companies to gauge their impact on social and environmental issues. In this article, we will discuss the concept of impact, its implications for organizations, and how it can be measured...

The most important and recent developments of ESG (Environmental, Social and Governance)

Being a B Corporation is not just about making profits and creating wealth for a company, it is a way of creating a more sustainable future for society! Discover our article about B corps and its benefits here...

The process for an enterprise to get the B corp certification

Becoming a B Corporation is an ambitious undertaking. This article will guide you through the steps required to become a B Corporation…

What is a B Corporation: what this means and its benefits for companies

Being a B Corporation is not just about making profits and creating wealth for a company, it is a way of creating a more sustainable future for society! Discover our article about B corps and its benefits here...

The guide to EcoVadis certification: frequently asked questions

This guide will take you through the steps of the EcoVadis Certification process, and explain what is involved in becoming a certified business...

The implications of ISO 26000 for companies

ISO 26000 is a standard providing direction for the application of social responsibility to the activities of an organization. But what does this mean? And how can organizations use it to create better and more sustainable business practices? Let's talk about it…

What is the meaning of CSR (Corporate social responsibility) and how to adopt it?

A Corporate Social Responsibility strategy refers to an organization's active consideration of the effects its activities have on the environment, employees, customers, and suppliers. Let's look at how your company could adopt such a program...

4 reasons companies should adopt CSR, Corporate social responsibility

CSR is all about managing a company’s externalities while creating sustainable value for stakeholders and continuous innovation for the business. Let's break that down and explore why...

Carbon disclosure project reporting: what is it and how does it work?

Read our article about The Carbon Disclosure Project (CDP), an extra-financial questionnaire that collects data on companies’ environmental practices and performance...

What are the differences between Corporate Social Responsibility (CSR) and Environmental Social Governance (ESG)?

These terms are both used to describe an approach for businesses to integrate social and environmental factors into their governance policies, strategies, processes, and programs. Yet, they're not the same. Let's explore their key differences...

Why is ESG (Environmental, Social and Governance) important for a business

ESG (environmental, social and governance) can help businesses make sound decisions, and investors achieve better long-term returns. Let's discover how...