Impact-washing - What is Impact-washing

Definition

The term “greenwashing” has been around since the 1980s.

Today, “impact washing” has been added to the lexicon of those seeking to hold companies and in particular financial institutions for their green claims.

Impact washing can be defined as any marketing claim about a product/good/services/funds triggering a change in the real economy that cannot be supported by evidence.

“Many financial institutions pretend that a change in the composition of their portfolio (such as reducing the exposure to the oil sector) automatically delivers environmental impacts,” explains Stanislas Dupré, Founder of the think tank 2° Investing Initiative and Convenor of the ISO working group that developed ISO 14097 (ISO 14097 is the standard “Greenhouse gas management and related activities – Framework including principles and requirements for assessing and reporting investments and financing activities related to climate change”).

“Today, impact washing is the norm rather than the exception. When my think tank reviewed the practices of asset managers in Europe in 2020, we found that many of them were making environmental claims and that almost all of these claims were misleading and non-compliant.”

How to stop impact-washing

To fight “Impact-washing” and to understand more deeply the impact of their investments on the populations served, investors can:

- not only require their investees to report on a set of common impact indicators but also run periodic in-depth impact studies, field visits, and partner on external evaluations and assessments

- evaluates its contribution to each of its investments based on an assessment of what would have happened in the absence of its investment

- set realistic, evidence-based targets, then monitor and evaluate actual achievements, using data and evidence to measure

A few tools have been created for governments, policymakers, and regulators to tackle the issue of impact washing:

- The standard ISO/TS 17033, Ethical claims and supporting information — Principles and requirements, which sets out internationally agreed ways to make a credible ethical claim

- The standard ISO 14097 - Greenhouse gas management and related activities — Framework including principles and requirements for assessing and reporting investments and financing activities related to climate change, which sets a benchmark for reporting financial institutions’ climate actions.

- The standard ISO 14021:2016 - Environmental labels and declarations — Self-declared environmental claims, which specifies requirements for self-declared environmental claims, including statements, symbols and graphics, regarding products. It further describes selected terms commonly used in environmental claims and gives qualifications for their use in order to avoid green washing.

In conclusion…

Demonstrating impact has not always been high on the agenda. However today, it is not enough anymore for all organizations, from governments to for-profit and nonprofit organizations, to simply say they are acting for the planet. They need to actively and verifiably demonstrate how they are doing it and give pieces of evidence.

Measuring their impact is crucial to prove environmental and social commitment to citizens, investors, stakeholders, employees, customers.

It will become the new standard so companies have to get prepared for the use of impact measurement frameworks and impact reporting.

In order to meet these demands, consolidation of methodologies, consistency in measurements and valuations and the increase in collaborations at a sector level to ensure comparability and transparency are expected in the coming years.

- ISO/TS 17033:2019 - Ethical claims and supporting information — Principles and requirements

- ISO 14097:2021 - Greenhouse gas management and related activities — Framework including principles and requirements for assessing and reporting investments and financing activities related to climate change

- ISO 14021:2016 - Environmental labels and declarations

ISO 26000 - What is ISO 26000

Definition

The ISO 26000: Guidance on Social Responsibility is the internationally recognized and supported standard for social responsibility, published by the International Organization for Standardization (ISO).

The standard defines social responsibility as: “ the responsibility of an organization for the impacts of its decisions and activities on society and the environment through transparent and ethical behavior” that:

- Contributes to sustainable development, including the health and welfare of society

- Takes into account the expectations of stakeholders

- Complies with applicable law and is consistent with international norms of behavior

- Is integrated throughout the organization and practiced in its relationships.

What is the intent behind ISO 26000?

ISO 26000 establishes the principles and guidelines of the concept of social responsibility.

It intends to help all types of organizations, like companies, NGOs, cooperatives, unions, operate in a socially responsible way and integrate socially responsible behavior into the organization. This means that organizations are aware of how their actions and decisions impact the people and the environment around them and act accordingly.

ISO 26000 is aligned with the definition of Corporate Social Responsibility (CSR) as defined in 2001 by the European Union: “A concept whereby companies integrate social and environmental concerns in their business operations and in their interaction with their stakeholders on a voluntary basis.”

Consequently, many organizations align their CSR strategy with the standard ISO 26000.

A quick history of the ISO organization and the ISO 26000 framework

Corporate social responsibility is not a new concept. The 1953 book ‘Social Responsibilities of the Businessman’ by Howard Bowen is often heralded as the start of the modern debate about the issues that organizations need to consider.

The consideration started with the organization’s philanthropic activity, and then gradually expanded over the years to include topics such as labor conditions, fair business operations, human rights, the environment, corruption, and consumer protection.

In response to this, the standard ISO 14001: Environmental management systems – Requirements with guidance for use, that focuses on pollution prevention and environmental management, was published in 1996. It is used by businesses, nonprofits, and government agencies to reduce pollution, waste, and greenhouse gas emissions.

Then, with the awareness of these subjects and the increase in the number of topics, the need for a wider framework appeared.

The ISO 26000 standard was published in November 2010. It is a result of 5 years of multi-stakeholders in-depth work. Over 400 experts from 80 different countries and groups such as industry, consumers, governments, labor, NGOs, service, support, and research have been involved.

Social responsibility is quite a complex concept. The ISO 26000 standard answers this issue providing guidance for organizations to implement sustainable development on a global scale.

ISO in numbers today:

- 24166 International Standards covering almost all aspects of technology and manufacturing have been issued

- 167 members representing ISO in their country. There is only one member per country

- 802 technical committees and subcommittees to take care of standards development

ISO 26000 today

Nowadays, ISO 26000 is one of the most widely used and recognized ISO standards.

The standard has been applied by tens of thousands of organizations of many types and sizes and in all parts of the world.

2020 marked ten years since ISO 26000’s first publication.

« Since publication ten years ago the standard has been adopted by more than 80 countries, most of which are developing countries, and we see how it has inspired public policy and businesses in Indonesia, Chile, India, China, Japan, the United Kingdom, Korea, the European Union among others. » Mr Staffan Söderberg, Vice-Chair of the ISO Working Group that developed ISO 26000, AMAP

Every few years, the ISO members body (160+ country members) is asked whether to keep it as it is, review or amend it, or withdraw the standard.

In the 2020/2021 review, the member’s body voted to keep ISO 26000 in its current version.

This review also highlighted some developments in the number of governments that have adopted ISO 26000: governments of Vietnam, Congo, Iran, Kuwait, Saudi Arabia, United Arab Emirates, and Sudan had reported having adopted or progressed the adoption. This brings the number of countries to 88.

However, while society has made progress in many areas over the last decade, the guidance of ISO 26000 remains more than relevant to addressing today’s challenges.

With many organizations being forced to reassess the way they do business in the light of COVID-19, the importance of social responsibility has come to the fore as a component of building a more resilient and more equitable business and therefore society.

Learn more about ISO 26000...

B Corp - What is B Corporation certification

Definition

B Corp Certification is a standard developed by B Lab, a nonprofit that certifies companies as being socially and environmentally responsible.

B Corp certification looks beyond a company’s financial performance to evaluate its environmental, social and corporate governance (ESG) criteria.

It includes, for instance, an assessment of the company’s policy for reducing carbon emissions caused by transportation, the percentage of management that comes from underrepresented populations, and the anti-corruption reporting and prevention systems it has in place.

In order to be certified as a B Corp, companies must meet high standards of social and environmental performance, accountability, and transparency; demonstrate a positive impact on society and the environment through their core values, business practices, and profits; and commit to using their growing influence as a force for good.

B Corp certification is managed by B Lab, which was created in 2006 by three former Stanford University roommates: Andrew Kassoy, Bart Houlahan, and Jay Coen Gilbert.

The organization was created after the founders realized that there was no way to understand whether a company was having a positive impact on society.

So they decided to change the system so that businesses could create value for all stakeholders—not just shareholders—and thus B Lab was born.

The certification process is time-consuming but the benefits are significant.

To learn more about B Corp...

B Corp key stats (as at October 2021)

- There are 4,088 B Corp-certified companies in 77 countries and 153 industries.

- 150 of these companies are in France and 430 are in the UK.

- More than 100,000 BIAs have been completed since 2006.

- Combined revenue of B Corps in the UK is £4.3 billion.

- Number of employees of B Corps in the UK is 22,000.

- Between 2017 and 2019, B Corp SMEs’ mean average annual turnover growth in the UK was 24%, compared to an average of 3% for all SMEs.

- 50% of B Corps have majority women management teams.

The concept of impact on social and environmental issues and its implication for companies

Measuring the impact of a company on social and environmental issues is a complex and important task, notably as it goes beyond mere reporting metrics.

Impact measurement covers different areas, such as avoiding harm or benefiting stakeholders, or contributing to solutions for social and environmental issues.

Impact measurement is essential to assess the achievement of sustainable goals, however, many still do not fully understand how to measure their impact or how to effectively manage it.

What does Impact mean?

In a business environment, there is a lot of ambiguity and confusion about what ‘impact’ is, how it should be defined, how to measure it, and what kind of measurement is sufficient.

Despite heightened attention paid to, expectations around, and use of the term impact, the concept does not have a shared definition of what it constitutes.

Impact has been defined by various international organizations.

The most commonly used definition of Impact being the one of the Impact Management Project which uses the same definition as the OECD: positive and negative, primary and secondary long-term effects produced by an intervention, directly or indirectly, intended or unintended.

As for Global Reporting Initiative: ‘impact’ refers to the effect an organization has on the economy, the environment, and/or society, which in turn can indicate its contribution (positive or negative) to sustainable development.

The term ‘impact’ can refer to positive, negative, actual, potential, direct, indirect, short-term, long-term, intended, or unintended impacts.

Principles and concepts

Objectives behind the concept of impact

Impact is a concept that is applied both prospectively and retrospectively to actions, programs, activities, and operations.

It aims to help organizations, profit and non-profit to:

- predict impacts at an early stage in project strategy, planning, and design

- decide whether or not to proceed with a planned course of actions

- decide whether to stop, continue, scale up or adapt an ongoing activity

- find ways and means to reduce adverse impacts and increase positive impacts

- shape projects to suit the local environment and take into account local communities

- present forecasting and options to decision-makers

Types of impact

Depending on their motivation on managing impact, organizations’ intentions range from broad commitments to more detailed objectives.

These intentions relate to one of three types of impact:

- At a minimum, organizations can act to avoid harm to their stakeholders. For example, decreasing their carbon footprint or paying an appropriate wage.

- In addition to acting to avoid harm, organizations can actively benefit stakeholders. For example, proactively upskilling their employees, or selling products that support good health or educational outcomes.

- Many organizations can go further — they can use their capabilities to contribute to solutions to pressing social or environmental issues. For example, enabling the underserved populations to achieve good health, or hiring and upskilling formerly unemployed individuals.

Source: Impact management project

Categories of impact

Impacts are related to environmental and social issues.

Organizations’ impacts will seat within one or both of those 2 categories:

1/ Environmental impact

When organizations’ decisions and day-to-day operations affect and influence:

- people’s environment: the quality of the air and water people use, the availability and quality of the food they eat, the level of hazard or risk, dust, and the noise they are exposed to, the adequacy of sanitation, their physical safety, their access to and control over resources…

- the natural earth system: disruption of the rain cycle, increase in land temperature, destruction of ecosystems, fauna, and flora, acidification of the oceans…

2/ Social impact

Social impact regroups all issues that affect people, directly or indirectly.

A convenient way of conceptualizing social impacts is to look at whether there are effects on one or more of the following:

- People’s way of life: how they live, work, play, and interact with one another on a day-to-day basis

Their culture, their shared beliefs, customs, values, and language or dialect - Their community: its cohesion, stability, character, services, and facilities

- Their political systems: the extent to which people can participate in decisions that affect their lives, the level of democracy in place

- Their health and wellbeing: health is a state of complete physical, mental, social, and spiritual wellbeing and not merely the absence of disease or infirmity

- Their personal and property rights, particularly whether people are economically affected or experience personal disadvantage which may include a violation of their civil liberties

- Their fears and aspirations: their perceptions about their safety, their fears about the future of their community, and their aspirations for their future and the future of their children

Organizations can conduct an Environmental Impact Assessment and/or a Social Impact Assessment, that includes the processes of analyzing, monitoring, and managing the intended and unintended environmental and/or social consequences, both positive and negative, of planned interventions (policies, programs, plans, projects).

Example of methodology to assess Environmental Impact: Carbon footprint at a company level, LCA at a product/service level, expert analysis…

Example of methodology to assess Social Impact: Surveys for all potentially affected people, case studies, expert analysis…

Impact in the investment industry

Today, more and more investors are talking about “impact”.

They are 3 types of investments that take sustainability and impact into account:

Environmental, social, and corporate governance (ESG)

It focuses on companies making an active effort to either limit their negative societal impact or deliver benefits to society (or both).

The 3 criteria, E, S, and G, constitute the three pillars of a company’s extra-financial analysis. Investors use the ESG approach to evaluate investees on expected practices (existing policies and actions on dedicated topics) and metrics (whether the company reports on certain KPIs).

ESG also provides a framework to assess the exposure of a company to sustainability ESG risks (through the lens of financial or double materiality).

Companies that meet ESG criteria do not necessarily demonstrate reduced negative impacts nor positive impacts.

For example, a company can have a climate policy in place and monitor its GHG emissions (as part of its ESG strategy) but still have a significant negative impact on climate change.

Examples of ESG investment: investing in a tech company that owns data centers using renewable energy, investing in a petrochemical company that has an ambitious climate policy.

Socially responsible investing (SRI)

It entails screening investments to exclude businesses that conflict with the investor’s values or that focus on businesses that prove to have the best environmental and social practices.

SRI can take different forms, including: ESG screening (invest in companies with the best ESG ratings), exclusion (excluding from the portfolio companies that do not respect international conventions or that operate in controversial sectors), and thematic approach (promoting investments in companies operating in the field of sustainable development).

SRI dates back to John Wesley, the founder of the Methodist movement in the 18th century, who urged his followers to avoid investing in “sin stocks” that generated profits from alcohol, tobacco, weapons, or gambling activities.

SRI goes further than ESG. Not only is SRI an investment that takes into account ESG criteria, but it is also part of a broader sustainable finance policy. All SRI-labeled funds usually meet ESG criteria. However, a fund that meets ESG criteria is not necessarily part of an SRI approach.

Examples of SRI investment: investing in companies operating in education, water, recycling, renewable energy, etc., divesting from fossil fuel and firearms industries.

Impact investing

It is a relatively recent practice, first mentioned in 2007 by the Rockefeller Foundation. It is characterized by a direct connection between values-based priorities and the use of investors’ capital. Impact investing meets a dual objective: to generate a substantial financial return and to create and quantify a positive societal impact.

Examples of impact investment: investing in an organization that contributes to building schools in underdeveloped countries, investing in a company whose core products help reduce GHG emissions (e.g. plant-based food), etc.

Impact investing mostly refers to private funds, while SRI and ESG investing involve publicly traded assets.

According to US SIF (The Forum for Sustainable and Responsible Investment), socially responsible investing (SRI), environment, social and corporate governance (ESG) investing, and impact investing assets grew from $3 trillion in 2010 to $12 trillion in 2018 to $17.1 trillion in early 2020.

Focus on the comparison between ESG and Impact Investing strategy

There is room for both ESG and impact investment strategies in the market, and investors may want to allocate funds to each in different proportions.

Both can deliver superior financial performance and make the world a better place, but they work in different ways, and there are some overlaps between the two strategies.

IFC provides a useful framework to understand the nuances between ESG and Impact Investing and compare actions taken at each stage of the typical investment process in the light of these differences:

Points of attention in the concept of Impact

Because the definition of impact is very broad and vast, it is almost impossible to propose a single, universal scope of application of the concept of impact.

There is currently no robust and recognized methodology for measuring net impact (positive externalities adjusted for negative externalities).

As a result, different perspectives and dimensions will affect how impact will be framed and measured by companies.

This leads to 2 points of attention when looking at Impact assessments:

- Organizations should be very attentive not to only focus on positive impacts and make sure to measure all negative externalities that can be generated and thus further mitigated. Impact data should be reliable, material, and account for both positive and negative impacts. Whichever tool and methodology organizations choose to employ, they should be transparent about the sources and the process used.

- It is not always relevant to compare different companies’ impacts. If done, the comparison must be carefully made, comparing data coming from the same tools and making sure the scope and methodologies are comparable (carbon footprint scope 1, 2, and/or 3 or LCA for example).

Reconciliation between ESG and Impact concepts

Created in 2016, the Impact Management Project (IMP) is the reference organization on impact measurement.

It provides a forum for building global consensus on measuring, assessing, and reporting impacts on people and the natural environment.

IMP is part of the organization that will advise the newly created International Sustainability Standards Board (ISSB).

ISSB was launched in November 2021 by IFRS to develop a comprehensive global baseline of high-quality sustainability disclosure standards.

ISSB aims at meeting investors’ information needs and supporting companies in providing transparent, reliable, and comparable reporting on climate and other environmental, social, and governance (ESG) metrics.

The integration of IMP into ISSB’s work is good news for organizations working towards impact but it might also blur even further the lines between ESG and Impact.

The most important and recent developments of ESG (Environmental, Social and Governance)

Environmental, Social and Governance (ESG) gained popularity in recent years, and is used by organizations to help them reduce financial, reputational and operational risks.

The purpose of ESG policy development is to ensure that companies do not harm the environment, society or governance, and to improve their impact. Which, consequently, improves their success in the long run.

However, ESG is changing.

ESG is set to grow rapidly and shape the corporate sustainability agenda. Here are some of the most crucial and recent developments.

Concentration in the ESG analysis industry

New types of rating agencies that focused on non-financial criteria began to develop in the early 2000s.

Rating processes were developed to help investors conduct in-depth analyses of the companies within their portfolios and how well those companies adhered to ESG criteria, and such agencies incorporated a review of a company’s environmental, social and governance (ESG) performance in addition to their economic performance.

These agencies are commonly called social and environmental rating agencies, or, extra-financial rating agencies.

Each extra-financial rating agency has its own evaluation grids and criteria, its own methodology. Just as there is a multiplicity of ESG standards and frameworks (GRI, IIRC, SASB, etc.), there are a number of different extra-financial rating agencies, each with their own process and ESG questionnaires.

Nevertheless, ESG rating processes are trending towards homogenization.

An initial consolidation movement (mergers, acquisitions or alliances) in the 1990s led to the appearance of the currently well-known extra-financial rating agencies operating on an international scope – Vigeo (France), MSCI ESG Research (United States), EIRIS (United Kingdom), oekom research (Germany), Inrate (Switzerland), Solaron (India) and Sustainalytics (Netherlands) – and the 2010s have seen continued consolidation, in a market increasingly dominated by American corporations.

Some of the most significant recent developments in the extra-financial rating ecosystem include:

- 2015 - Vigeo merges with Eiris

- 2018 - Oekom Research is acquired by ISS

- 2019 - Vigeo-Eiris is acquired by Moody’s Corporation and becomes V.E.

- 2020 - Sustainalytics is acquired by Morningstar

ESG funds

ESG funds are growing rapidly, indicating huge market demand for application of ESG strategy.

CNBC puts ESG fund inflow at over $21 billion during the first quarter of 2021, an increase from the $51 billion for the entire year of 2020 and $21.4 billion in 2019.

A BlackRock representative attributes this increase in interest for ESG to more visibly impactful methods of incorporating sustainable investments. Financial experts now view ESG as a “core-type strategy”- and this trend looks like it will only continue in the coming decades.

Data and Tech in ESG evaluations

ESG leaders are still struggling to get a hold on the unwieldy world of ESG data, but the standardization of ESG reporting and disclosure is of high priority.

ESG analysts from Forrester suggest that industry regulations will become increasingly specific, detailed, and relevant in coming years. Companies are also reacting to dynamic materiality and the unpredictability of factors like new knowledge, regulations, and global events by adopting and developing new procedures to measure risk.

Market reactions to the climate crisis

According to the most recent IPCC climate report, the world has reached an increase of 1.1°C compared with the average in 1850–1900, resulting in extreme weather such as the 2020 Australia wildfires.

In order to achieve the Paris Agreement limit of a 2°C increase by the end of the 21st century, MSCI’s Warming Potential estimates that every company in the MSCI ACWI IMI would have to reduce total carbon intensity (Scopes 1, 2 and 3) by an average of 8%-10% per year from 2021 until 2050.

The need for steep reductions in emissions in portfolios means that companies would have to find means of decarbonizing rapidly, and investors/investment firms are faced with the choices of convincing companies to undergo massive overhaul of procedure, change their portfolio concentration, and/or shift assets.

In conclusion…

The need for ESG only seems to be growing as society enters unprecedented times: climate change, protests and social upheaval, increasing technological capabilities, the ongoing COVID-19 pandemic.

The lack of existing data on the situations that we now face make clear a need for frameworks that can quantify and mitigate unpredictable risks.

ESG strategies can help meet those needs, while providing some guidelines on how to build more resiliency into the corporate universe.

So, what are you waiting for? Start implementing ESG today!

And this is where we can help:

If you want to succeed in your sustainable journey: save time, get organized, and stay compliant with our tool!

Thanks to our AI, apiday provides you with a simple and efficient process for your data collection, verification, reporting, and certification.

Get your organization started and book a call with our ESG experts!

The process for an enterprise to get the B corp certification

B Corps are for-profit companies that have been certified by the B Lab to meet rigorous standards of social and environmental performance. The mission is to redefine success in business so that it works for all stakeholders.

In these times when more and more people care about the impact of their consumer choices, to be certified as a B Corporation makes complete sense. But what are the steps to becoming a B Corp? How can you get help? This article will cover it all.

Becoming a B Corp: The process

1. Go to the website: bimpactassessment.net

2. Complete the BIA.

2a. If you receive a score of under 80 (of a possible 200) points, the adventure ends here.

2b. If you earn a score of 80 or above, you are able to submit your assessment (once you’ve paid the submission fee).

3. Schedule a review call with a member of the B Lab team using the email sent to you a few days after your BIA submission.

4. At least 2 business days before your review call, upload the supporting documents for 6 to 15 randomly selected questions.

5. Attend the 60- to 90-minute review call to look over your answers to the assessment and the documentation provided, during which your score will likely be adjusted.

5a. If your final score is lower than 80 points, the adventure ends here.

5b. If your final score is 80 or above, you will receive a list of additional documents to be provided for a further set of questions (up to 6).

6. Complete the disclosure questionnaire.

7. Use the legal requirement tool to determine how you can integrate stakeholder consideration into the governance structure of your company, depending on its structure and location.

8. Sign the B Corp agreement, which lasts for 3 years and includes the interdependence declaration.

9. Pay the annual fees, which are based on the most recent annual revenue of your company.

Please note that this process can vary depending on the size of your company.

Onsite visits can, for example, be added for large companies.

Timeline and costs

The review process takes on average 6 to 10 months to complete, but due to the growing popularity of the certification and the steady increase in the number of applicants over the past couple of years, it can now take more than a year to complete in some instances.

With regard to fees, as at 2021, the BIA submission fee for businesses in the US and Canada is $150, with the annual certification fees costing $1,000-$50,000, depending on the annual revenue of your company (it can be more for companies with an annual revenue higher than $1 billion).

Tools and resources

The BIA

Using a multiple-choice questionnaire, the BIA assesses the impact of both your company’s day-to-day operations and its business model.

Help is provided for each question, such as definitions of terms, examples of companies who have already dealt with a particular topic, and best practice guides.

The assessment comprises about 200 questions that are tailored according to your company’s size, sector, and location.

Gathering and creating the documents needed to fill out the BIA takes on average 100 hours for a startup or small and medium-sized enterprises (SME) with no existing ESG data management software.

It takes then 1 to 3 hours to complete the BIA itself for a small company, but it can take longer depending on the size, age, and complexity of the company.

Questions addressing the company’s operational impact

Some samples of BIA questions can be found for each category, as below:

- How does your company integrate social and environmental performance into decision-making?

- Which of the following anti-corruption reporting and prevention systems are in place?

- What percentage of your company is owned by full-time workers (excluding founders/executives)?

- Based on referenced compensation studies, how does your company’s compensation structure compare with the market?

- How does your company engage and empower workers?

- What percentage of management is from underrepresented populations? (This includes women, minority/previously excluded populations, people with disabilities, and/or individuals living in low-income communities.)

- Does the company currently use any of the following specific practices to reduce carbon emissions from transportation?

- What percentage of energy used is from renewable on-site energy production for corporate facilities?

- Questions addressing the impact of the company’s business model

Depending on your answers to the gating questions, your company’s business model may also be evaluated in the BIA in a series of questions that can, in most cases, add up to 30 points to your score.

The questions usually focus on evaluating the intensity and relative magnitude of the impact of your business model, but some weighted and unweighted questions about the impact measurement and management are also included.

Specific questions about how your organization is managing the outcomes produced by the model might also be asked.

It must be noted that some of the calculations are automatically done based on the answers to previous questions.

Questions addressing disclosure

After completing 90% of the BIA, you will be asked disclosure questions about potential negative impacts.

Any sensitive information disclosed by your company about fines, sanctions, material litigation or sensitive industry practices on your records is handled confidentially by B Lab and does not directly affect your score.

However, the Standards Advisory Council and B Lab’s Board of Directors reserve the right to deny or revoke certification if a company’s previous behavior does not fit the spirit of the community.

Finally, a background check of your company and senior management team and a public complaints process is carried out by the B Lab team.

Best practice guides

Two main best practice guides are available for free on the B Corporation website to help candidate companies with the overall comprehension of the certification process and requirements: One is dedicated to small to medium-sized companies and the other to large companies.

There are also best practice guides that cover more specific topics, such as how to engage and retain a diverse workforce and how to build engagement and accountability through transparency.

Other guides provide companies with tips for and examples of how to best implement practices such as monitoring water use or conducting supplier surveys.

Once a company becomes B Corp certified, it receives access to the full catalogue of documentation and best practices available via the B Hive online platform to help improve its impact score.

Logging on to this tool also allows B Corps to connect and collaborate with the community and benefit from discounts offered by other members and partners, as well as find out about other B Corps’ products and services.

Improvement reports and case studies

After completing the BIA, companies will receive a tailored improvement report proposing a timeline of actions to be implemented within 1 to 6 months, 6 to 12 months, and 12 months plus, so that they can increase their score.

Some case studies of businesses who managed to increase their score subsequently are also available, allowing companies looking for inspiration to see what practices others are implementing.

Other resources

The B Corporation website also offers free access to an employee handbook template, as well as external resources including The B Corp Handbook and videos explaining how to improve your BIA score.

A B Climate Tools Base, which curates documentation and tools from different organizations to help companies take action on environmental aspects, is available online as well.

More than 350 reports, as well as interactive tools, case studies, online courses, policy documents and podcasts can be found on this website.

In addition, B Corp-certified companies can participate in various challenges, such as 2019’s call to action for an inclusive economy, and receive access to dedicated internal and external resources to help them achieve the expected metrics.

These resources include guides on how to grow a diverse workforce, guidelines on how to set gender diversity targets, and an introduction to web accessibility.

How to get help

B Leaders

B Leaders training programs have been created in the UK, France, and many other regions to support candidate and B Corp-certified companies needing help in getting to grips with B Corp terminologies, tools, and processes.

Training typically includes sessions dedicated to the understanding of the B Corp ecosystem, advice and tips on using the latest version of the BIA tool, as well as a step-by-step review of the certification process.

Some practical cases are also presented to trainees as a way of sharing best practices on how to engage internal and external stakeholders, improve their company’s score, and communicate the company’s impact performance.

This training also provides a good opportunity to meet B Corp-certified companies that are willing to share their experiences.

Prices for the program start at $500 for one person, rising to $20,000-$30,000 to train all the people in the company who are involved in the B Corp-certification process.

External tools

The application process for B Corp can be intimidating and time-consuming.

Not all companies can dedicate time to figuring out what documents are needed for filling the forms, and even if the companies do, does it mean the information is accurate?

A lack of documentation and accuracy in the audit phase could compromise the certification process.

And that’s why we created apiday! To help you streamline your processes.

Our artificial intelligence software can complete applications in no time, saving you months of work. Just send us all the required documents, we’ll handle the rest!

CSR - What is Corporate Social Responsibility

Understanding CSR

What is the definition of CSR?

CSR stands for Corporate Social Responsibility.

The European Commission defines CSR as “a concept whereby companies integrate social and environmental concerns in their business operations and in their interaction with their stakeholders on a voluntary basis”.

In short, CSR is centered on the idea that businesses have a responsibility to benefit the society that they exist within—a broader view than the one that says businesses’ only responsibility is to produce economic profit.

How does CSR work?

Corporate social responsibility is a form of self-regulation and can be highly individualized; CSR strategies and activities will vary according to the company in question.

CSR activities are generally not mandated— even though there are more and more regulations on CSR – they are voluntarily undertaken by companies to assess and mitigate impact on society and the environment, as well as to give back to society and reap the benefits associated with creating positive social value (such as improved risk management and higher employee engagement).

CSR practices are often guided by a concept called the “Triple Bottom Line,” which encompasses economic, environmental, and social imperatives in the journey towards positive impact.

CSR Key Concepts and Terms

CSR categories

CSR categories (and subcategories) may differ depending on the regulating body and/or the corporation in question, and classification has changed over the course of time. However, the three broadest and most generally accepted categories are: environmental, social, and economic.

- Environmental: corporations, especially the larger corporations and companies in specific industries, can significantly damage the environment via greenhouse gas emissions, pollution, and resource depletion.

Accepting environmental responsibility means committing to monitoring activities that are potentially detrimental to the environment, and preventing negative environmental impacts. This concept is sometimes also known as environmental stewardship. - Social: ethical responsibility in business means fair business practices—ensuring that all people involved in the corporation’s activity (ie. employees, suppliers, consumers and other stakeholders) are treated fairly and with respect (non-discrimination, workplace safety, products safety, local procurement, etc.).

- Economic: economic responsibility means making financial decisions that considers a greater good and that takes into account the impacts of activities, rather than keeping a narrow focus on making as much money or saving as much money as possible.

Note that while these categories are distinct, they are not mutually exclusive. There are often areas of overlap among the four categories.

Examples of CSR considerations

| Environmental | Social | Economic |

|---|---|---|

| Implementation of a recycling program | Competitive wages and benefits | Investing sustainably |

| Waste or pollution reduction systems | Ethically sourcing materia | Fair trade practices |

| Introducing renewable energy initiatives | Improving labor standards | Transparent supply chain |

| Engaging in a net zero strategy | Improving diversity, equity, and inclusion (DEI) | Philanthropy |

Individual CSR frameworks may also independently establish categories.

For instance, the ISO 26000 identifies seven core subjects (see below), as well as seven key principles focusing on accountability, transparency, ethics, stakeholder interests, human rights, laws and norms.

- Organizational governance

- Human rights

- Labor practices

- Environmental responsibility

- Fair operating practices

- Consumer protection

- Community involvement and development

Principles of CSR

Organizations sometimes create guiding principles (sometimes conflated with CSR responsibilities) for CSR activity.

Note that as with the CSR categorization of responsibilities, there is some variance in which principles are selected. According to research by Crowther and Aras (2008), some basic principles are:

Sustainability

In line with the United Nations’ definition of sustainability—using resources in such a way that future generations may continue to benefit from those same resources.

Accountability

Recognition and acceptance of the fact that the corporation has an impact on its external environment, and a responsibility for the effects of its actions.

Accountability also implies a commitment to quantification and reporting out of impact. Crowther and Aras further define characteristics of good reporting; it must be:

- Understandable to all parties concerned

- Relevant

- Reliable (accurate, representative, and free from bias)

- Comparable (consistent and replicable)

Transparency

All relevant information—ie. relating to the effects of the corporation’s actions—should be readily apparent and not misleading.

Recent Developments

Evolution of CSR Regulations

In 2014, the European Parliament adopted provisions that required some companies (with over 500 employees) to disclose information on their CSR operations and activities, making impact reporting a clear obligation along with the standard financial reporting.

At the time, the three key EU regulations on sustainability disclosure were the EU Taxonomy, the Sustainable Finance Disclosure Regulation (SFDR) and the Non-Financial Reporting Directive (NFRD).

These regulations defined scope of reporting and required activities, with some overlap between the three regulations.

In 2021, the European Commission (EC) adopted a proposal for a Corporate Sustainability Reporting Directive (CSRD) that amended reporting requirements of the NFRD and effectively updated the directives of the aforementioned regulations.

Key things to know about the CSRD proposal is that it:

- Extends the scope of the NFRD

- Requires an audit of reported information

- Introduces more detailed reporting requirements (refers to mandatory EU sustainability reporting standards), and

- Requires companies to make reported information accessible to a shared access point.

Evolution of CSR Topic Focus in Corporations

In light of sobering climate change statistics—the IPCC reports that many extreme weather developments are irreversible now—more and more corporations are recognizing various social and environmental issues as material and are increasing efforts to address and prioritize such topics.

The recognition and perhaps increased commitment to the Triple Bottom Line are evident in larger numbers of corporations attending recent global summits such as COP26 and the IUCN Congress.

The heightened scrutiny of issues that fall within the purview of CSR has led to an evolution in the sort of CSR expertise required.

Companies are now diversifying with CSR experts; as the field of CSR continues to expand, CSR professionals are increasingly specializing in specific topics and are hired to work on dedicated topics, rather than needing to serve as general advisor for all CSR issues.

Some of the biggest issues currently include climate change, biodiversity, and human rights/labor rights.

CSR vocabulary

- Materiality: “An organization's significant economic, environmental and social impact… issues that substantially influence the assessments and decisions of stakeholders.” Definition from NYU Stern

- ARO approach: ARO stands for avoid, reduce, and offset– the three steps, in order of priority, that define sustainability efforts, especially with regards to emissions and resource conservation.

- Sustainable Development Goals: A set of 17 interlinked global goals that were designed by the United Nations as a blueprint for a better and more sustainable future.

- Triple P’s (People, Planet and Profit): Also commonly called the ‘Triple Bottom Line,’ this business framework expands business success metrics beyond immediate profit to include a focus on environmental and social impacts as well.

- Ethical Consumerism: A form of activism wherein consumers choose or reject products based on the practices and values of the company producing the product.

- CSR Verification: According to the CSR Implementation Guide, verification is “a form of measurement that can take place in any number of ways: internal audits, industry (peer) and stakeholder reviews, and professional third-party audits”. Going through the verification process is a best practice for CSR activities because verification strengthens transparency and accountability around CSR.

- Stakeholder theory: The basis for the stakeholder theory is similar to the basis for CSR—the idea that companies should create widespread value, not just for shareholders. The stakeholder theory highlights the varied relationships between all groups and individuals impacted by the corporation in question, and holds that these relationships should create positive value. Examples of potential company stakeholders might include: employees, customers/clients, suppliers, the local community, and public authorities.

What is a B Corporation: what this means and its benefits for companies

A B Corporation is a for-profit entity that is committed to creating a beneficial impact on society and the environment.

Companies can take this commitment by becoming certified through the nonprofit organization B Lab, by meeting rigorous standards of social and environmental performance, accountability, and transparency. Being a B Corporation has many benefits for companies as it is well-regarded by investors, customers and employees.

What is B Corp

B Corp certification: an ESG certification

B Corp sustainability certification looks at various environmental, social and corporate governance (ESG) criteria to assess a company’s performance beyond sole financial results.

It includes for instance an evaluation of the company’s policy for reducing carbon emissions caused by transportation, the percentage of management that comes from underrepresented populations, and the anti-corruption reporting and prevention systems it has in place.

B Corp certification: A force for good

Certified B Corps commit to using their profits and growth to have a positive impact on the world.

As stated in the B Corp declaration of interdependence, they must conduct their business as if people and places matter, and should aspire to do no harm and benefit all through their products, practices, and profits.

Therefore, B Corp certification doesn’t simply assess a product or a service sold by a company but rather its broader impact on society and the environment.

B Corp certification: a B Lab certification

B Corp certification is managed by a non-profit organization called B Lab, which was created in 2006 by three former Stanford University roommates: Andrew Kassoy, Bart Houlahan, and Jay Coen Gilbert.

After several years spent running a sporting goods company, Houlahan and Coen Gilbert realized through discussions with Kassoy, who had been working in private equity, that there was no way to understand whether a company was having a positive impact on society.

So together they decided to change the system so that capitalism could create value for all stakeholders, not just for shareholders.

Who is B Corp certification for?

B Corp-certified companies: Eligibility criteria

Only for-profit companies that have been up and running for at least for 12 months are eligible for B Corp certification.

Companies and startups less than one year old are eligible for Pending B Corp status, for which they need to comply with B Corp legal requirements and fill out an indicative BIA, which will not be reviewed before the company’s first anniversary.

Companies that are publicly traded or have between $100 million and $4.9 billion in annual revenue, and large multinational and parent companies that have more than $5 billion in annual revenue, are also eligible for B Corp certification, but will have to follow a slightly different process as there will be additional considerations and requirements.

Parent companies with subsidiaries, subsidiaries themselves, affiliated entities and franchises are subject to the same requirements.

An important element to consider before starting the B Corp application process is to make sure you have the support of all your company’s teams, including management and the board.

Building a strong lead team that encompasses people from a selection of departments along with a dedicated project manager and a timeline is also essential.

And discussions with the leadership team and the board must take place before starting the process in order to ensure everyone understands and agrees with the level of transparency and the changes to the articles of incorporation that will be required.

What are the benefits of B Corp?

Better resilience

According to a study published by Deloitte in 2021, 87% of surveyed C‐level executives and senior public‐sector leaders who declared they have done very well at balancing the needs of all their stakeholders also felt that their companies could quickly adapt and pivot in response to disruptive events.

More specifically, according to this research, organizations with good reputations for valuing their workforces, helping communities, and being transparent with stakeholders on ESG issues are more likely to score highly on key resilience indicators.

Attracting and retaining talent

Being a B Corp-certified company helps to recruit and retain employees.

A 2016 study carried out by LinkedIn and Imperative found that purpose-driven companies get more engagement on LinkedIn, with a 33% higher InMail acceptance rate and 3.5 times more followers per employee.

In addition, it revealed that 74% of LinkedIn members place a high value on finding work that delivers on a sense of purpose, and that those purpose-oriented workers are more likely to stay at a company for more than 3 years than non-purpose-oriented workers.

Alignment with customer values

A NielsenIQ study published in 2015 found that 66% of respondents were willing to pay more for products and services that come from organizations that are committed to having a positive social and environmental impact.

B Corp certification is a trustworthy label, with high standards that flag to consumers that the company is committed to considering the impact of its decisions on its workers, customers, suppliers, community, and the environment.

Easy networking

Obtaining the B Corp certification also means joining a community of companies that share the same values and can potentially become partners.

B Lab supports the community with B2B peer circles—groups composed of B Corps that have the same best practices and ideas on a range of topics. In addition, certified B Corps gain access to discounts via the B Hive platform.

Enhanced investor attraction

As detailed in a Morgan Stanley report from 2018, assets under the management of signatories of the Principles for Responsible Investment (PRI) have risen exponentially from 2006, reaching $68.4 trillion.

This United Nations-supported network has attracted rising numbers of investors thanks to its systematic and explicit inclusion of material ESG factors in investment analysis and decisions.

Indeed, investors are now more aware than ever that managing environmental and social factors is simply part of sustaining competitive advantage in today’s economy and can mitigate risk events, and are increasingly wanting to align their personal values with their investments.

Becoming a B Corp: The methodology

B Corp certification hinges on 5 evaluation categories—governance, workers, community, environment, and customers—which examine different elements of a company’s policies, as below.

- Governance: the company’s mission, stakeholder engagement, ethics, and transparency.

- Workers: employees’ financial security, health, wellness and safety in the workplace, career development, engagement, and job satisfaction.

- Community: the organization’s diversity, equity and inclusion, economic impact, civic engagement and contribution to society, and supply-chain management.

- Environment: the company’s environmental management and how its business practices impact surrounding air, climate, water, land, and life forms.

- Customers: customer stewardship through sales and marketing and ensuring the best customer experience.

As part of their application for B Corp certification, companies must complete a B Impact Assessment (BIA), available for free online, which involves answering roughly 200 questions about the topics addressed by these categories.

The standards used in the BIA are overseen by B Lab’s independent Standards Advisory Council and updated every year.

The guide to EcoVadis certification: frequently asked questions

What is EcoVadis?

Created in 2007, EcoVadis provides a collaborative web-based rating platform assessing the non-financial global performance of organizations, working towards increased insight into the sustainability performance of their suppliers.

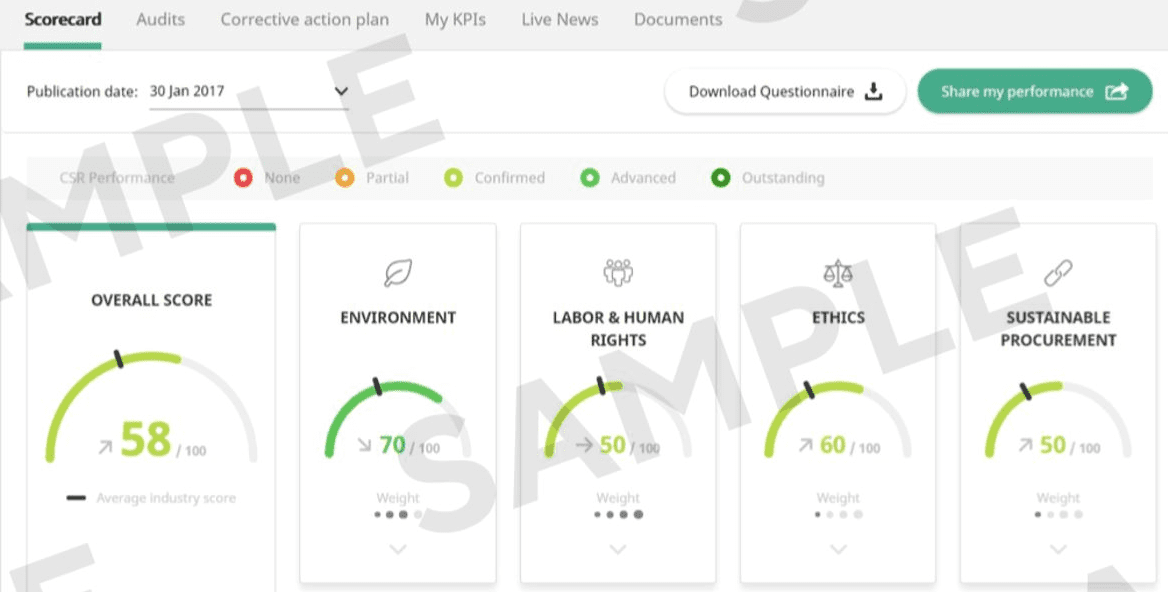

The non-financial assessment by EcoVadis measures the sustainability management system of a company through 21 sustainability criteria focused on four key performance areas:

- Environment: impact from the production processes (energy consumption, water, biodiversity, local and accidental pollution, GHG emissions), impact from product use, and end-of-life

- Labor & Human Rights: Human resources management (accident prevention, staff training, working conditions, social dialogue) and Human Rights (respect for labor laws, diversity, discrimination)

- Ethics: corruption, anti-competitive practices, and information management responsibility

- Sustainable procurement: supplier environmental and social practices.

Source: EcoVadis, methodology

The methodology is based on international sustainability standards such as the Ten Principles of the UN Global Compact, the International Labor Organization (ILO) conventions, the Global Reporting Initiative (GRI)’s standards, the ISO 26000 standard, the CERES Roadmap, and the UN Guiding Principles on Business and Human Rights, also known as the Ruggie Framework.

The methodology also integrates sustainability regulations from +160 countries.

The evaluation is driven according to 7 EcoVadis founding principles:

- Evidence-based: the rated company must provide evidence and supporting documents and is responsible for them (strategic notes, certificates, reports)

- Industry, location, and size matter: the assessment takes into account specific issues related to the sector, presence in risky countries, size, and geographic scope

- Diversification of Sources: The rating takes into account standpoints published by NGOs, trade unions, international organizations, local authorities, or other third-party organizations (e.g., auditors, CDP, external compliance database)

- Technology is a must: the EcoVadis IT system integrates learning, growth, rapid scalability and facilitates industrialization

- Assessment by International Sustainability Experts: the documents are analyzed by an international team of experts up to date with the latest best practices in sustainability

- Traceability and Transparency: the documents are stored securely and can be traced back. Rated companies may access to the most detailed results and to each scoring decision

- Excellence Through Continuous Improvement: EcoVadis has implemented and operates a company-wide quality management system supported by a client advisory board and a scientific committee.

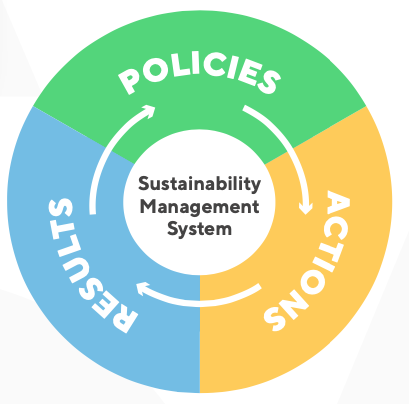

For EcoVadis, an effective sustainability management system relays on three management layers Policies, Actions and Reporting On Results, separated into seven management indicators: Policies (POLI), Endorsements (ENDO), Measures (MESU), Certifications (CERT), Coverage – Deployment of Actions (COVE), Reporting (REPO) and 360° Watch Findings (360).

Who is EcoVadis for?

The EcoVadis rating is available to all companies and suppliers, excepting the companies operating in Manufacture of tobacco products (ISIC code 1200), Mining of coal and lignite (ISIC division 05), Manufacture of weapons and ammunition (ISIC code 2520), Manufacture of air and spacecraft and related machinery (ISIC code 3030).

The EcoVadis company users can be:

- Either a client company whose procurement executives request their suppliers to answer EcoVadis. Then they get access to easy-to-use scorecards and are allowed to monitor the sustainability performance of their business partners as well as their continuous improvement actions.

- Either suppliers that are requested to answer a client's request. After being rated, the suppliers may share their scorecard results with the member community or other share on the platform. This possibility may increase their business opportunities. This sharing requires their authorization, and the platform ensures the confidentiality of their sensitive information.

In total, EcoVadis covers more than 200 purchasing categories.

Is EcoVadis to be responded to on a group or subsidiary level?

The EcoVadis assessment scopes allow participation at various organizational levels, from group levels (headquarters, holding, or parent company) to subsidiary levels (business unit, country-specific entity, manufacturing site, or regional operating company).

On a group level, the documentation provided has to cover all the underlying entities to avoid the risk of a lower score. For instance, in the case of a company ISO certified for an entity in a country, but not in other countries, it may be more beneficial to conduct the assessment on a subsidiary level in a country where the company is ISO certified.

Conversely, large companies with an overarching management approach or requested to complete the survey on multiple entities can process the assessment at the group level, as long as they can provide supporting documentation at this group level as well.

Why is EcoVadis important?

What are the benefits for for profit companies ?

The use of technology is a key part of EcoVadis assessment: the collaborative, integrated web-based platform helps monitor the sustainability performance of suppliers with reports and dynamic quantitative metrics.

For each of the four sustainability themes (Environment, Labor & Human Rights, Ethics, Sustainable Procurement), the easy-to-use scorecards give a clear, dynamic view on a company’s performance: insufficient, beginner, intermediate, advanced, and leader. This information helps to implement prioritized actions to focus on for improvement.

Since 2021, a dedicated and independent scorecard for Carbon has been added.

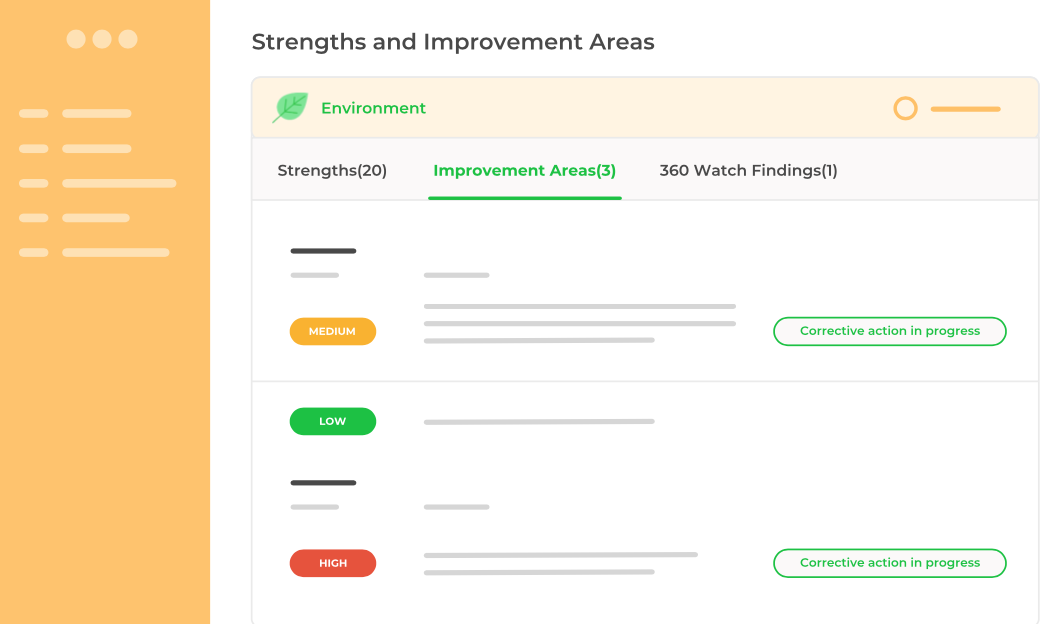

More qualitatively, strengths & improvement areas provide more details and insights into a company’s score, as in the figure below.

Source: EcoVadis, Strength and Improvement areas, https://ecovadis.com/suppliers/

Improvement areas are automatically added to the company’s Corrective Action Plan, pre-organized by priority.

The Corrective Action Plan (CAP) is a tool shared between the evaluated company and its client, in order to improve the CSR performance.

It is strongly recommended when the supplier’s score is below 47, choosing the 5-10 most important actions that are automatically proposed by the tool.

Uploading new documents does not impact the current scorecard, but will be considered for the next re-evaluation.

Unlike other ESG rating agencies, the EcoVadis assessment is built on thorough documentation analysis by a global team of sustainability experts from 50+ nationalities who will verify whether the company answers are supported by the proper documents and respect criteria.

How long is the recognition valid?

EcoVadis scorecards are valid for 12 months after publication.

Once the 12 months have passed, the company will still be able to access its scorecard (and the ones of suppliers) but will no longer be able to share the results publicly.

Companies subscribe to an annual fee ranging from €350 to €6,500, depending on the company size.

This subscription covers the EcoVadis assessment, access to the EcoVadis platform and resources, and the ability to share the company’s performance.

What is an EcoVadis rating? The step-by-step process

The EcoVadis assessment process takes place in 4 phases.

Source: https://ecovadis.com/suppliers/

Step 1: Registration on the EcoVadis website

The client is asked to create a company profile specifying the business activity and the contact information.

Step 2: Questionnaire

Once the registration is complete, a link and instructions (e.g. deadline to complete the questionnaire) are sent to create the account and access the platform.

The EcoVadis assessment can be conducted in 8 languages: English, French, Spanish, Dutch, German, Italian, Portuguese, and Chinese.

Documents can be submitted in all languages but it is preferable to upload documents in one of these languages, especially English.

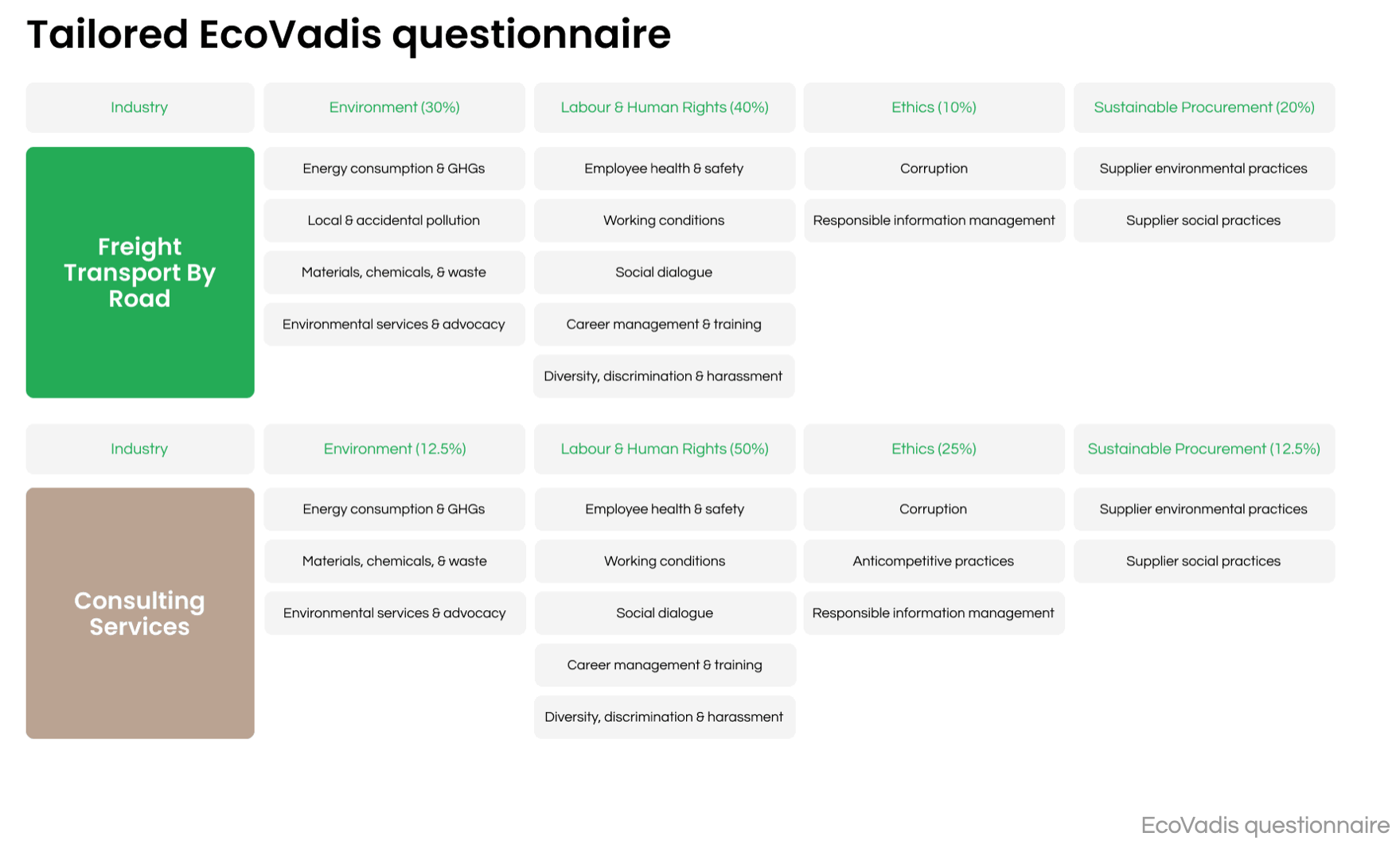

According to the company sector, size and country, a tailored questionnaire is built by EcoVadis, and the procurement executives can request their suppliers to undergo the assessment throughout the platform.

Source: Nexioproject, The Ultimate Guide To EcoVadis

From the dashboard, the control panel displays which criteria are activated for the company evaluation and their level of importance: not activated, activated with medium importance, activated with high importance, or activated only in risk countries.

Step 3: Expert analysis

After filling out the questionnaire, EcoVadis ESG experts will assess the answers and the supporting documentation.

The process takes approximately 6 to 8 weeks, depending on the complexity of the information provided by the company and the number of documents submitted.

For this step, EcoVadis Analyst not only reviews answers and documents provided by the company but also external resources (media, NGOs, etc.).

Step 4: Results

Once the answers are analyzed and results published, the platform notifies the company via email.

EcoVadis rating methodology

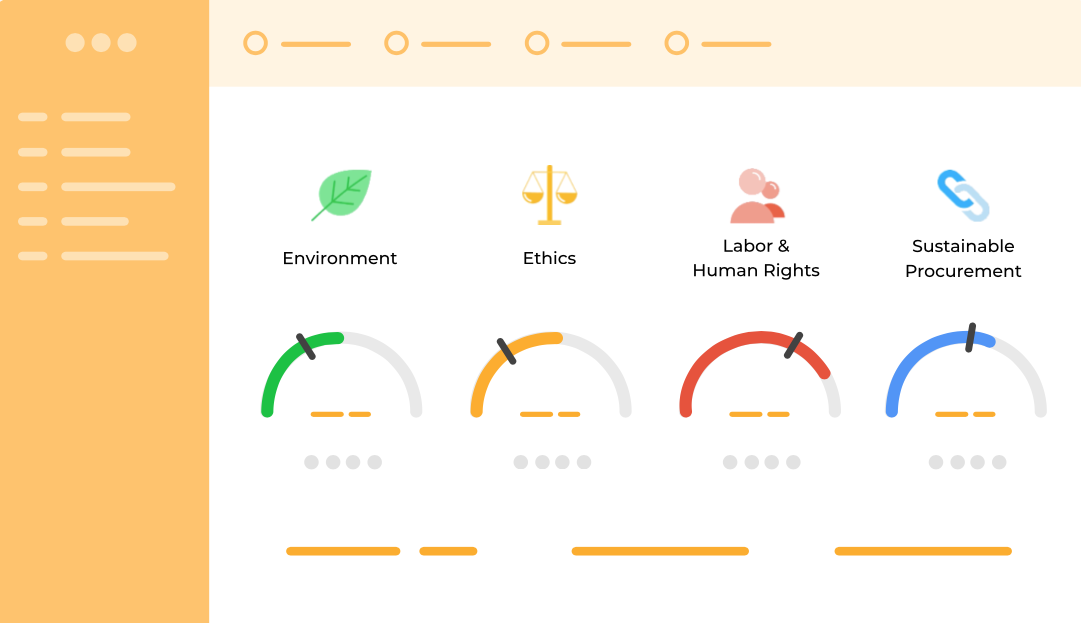

An overall final score out of 100 is given to the company.

It is a weighted average score, function of the size, industry and location of the company, on the four themes (Environment, Ethics, Labor & Human Rights, Sustainable Procurement).

This overall score reflects the quality of the company’s and its supplier network’s sustainability strategy, actions, and performances at the time of assessment.

The three management layers are given the following weights: policies account for 25% of the scoring, actions for 40% and results for 35%.

Source: https://ecovadis.com/suppliers/

The company scorecards can be easily shared with employees or customers and compared against peers in the industry, thanks to EcoVadis’ benchmark (see example below).

Example of a company’s benchmark performance (part of the EcoVadis scorecard)

Once the results are calculated, the company might receive an EcoVadis medal based upon the percentile rank of its score.

This percentile rank is calculated across all assessed companies in all industries, not per industry.

In January 2022, the reviewed criteria are as follows:

- Platinum - top 1% (overall score between 75 and 100)

- Gold - top 5% (overall score between 67 and 74)

- Silver - top 25% (overall score between 56 and 66)

- Bronze - top 50% (overall score between 47 and 55)

The medal shows the year in which the assessment was completed and can be used as external recognition on the company’s website and on communication to investors, trading partners, and customers.

The detailed rating methodology is available on EcoVadis’ website.

How to prepare for EcoVadis certification?

First assessment

The better prepared a company is, the easier it will be to complete the assessment process.

Each of the four themes covered is generally assigned to a specific department: Environment to the Corporate Social Responsibility (CSR) manager, Labor & Human Rights to Human Resources (HR) manager, Sustainable Procurement to the Procurement team, and Ethics section to the IT or Legal departments.

One person within the company should be appointed as being responsible for the overarching questionnaire, for collecting relevant documents and making sure they answer EcoVadis’ requirements.

The EcoVadis website provides some general guidelines and dedidated webinars to help companies understand its requirements.

For premium customers, the eLearning platform EcoVadis Academy offers introductory and advanced online courses in five languages (English, French, German, Spanish, and Chinese) aligned with the EcoVadis rating methodology.

The EcoVadis Academy enables administrators to track individual progress, monitor, and assign coursework to drive supplier sustainability improvement programs identified within a company’s scorecard.

Reassessment

The reassessment process may be initiated when the scorecard has expired or when the minimum score requested by a partner has not been reached.

Before starting reassessment, it is recommended that 1- the company reviews guidance provided within its previous scorecard, and 2- establishes a progress report, based on the corrective actions implemented following previous assessment.

Tips on how to ensure the best score

Supporting documentation requested by EcoVadis are crucial elements of the assessment.

Hereafter is a check-list to effectively prepare for the process:

- All documents must contain the company name, logo, date of implementation, and/or review date. All languages are accepted. Authenticity is key: if a document is created for satisfying the EcoVadis questionnaire, it will not be accepted.

- Policy documents should contain qualitative and/or quantitative objectives and pre-exist for more than three months before being uploaded on the EcoVadis platform. The validity period for a policy is eight years.

- Documents supporting actions should describe their function and how they contribute to the mitigation of relevant risks. Their validity period is eight years.

- Results: the validity of a reported KPI is two years.

EcoVadis allows a maximum of 55 new document uploads for one assessment.

Options for facilitation and aid from third-parties

Getting through EcoVadis assessment is complex and time-consuming. Most companies lack the expertise to complete it on their own and are prone to mistakes that could complicate matters further. But we can make everything smoother!

With apiday, there is an easier way. 🌿

Our AI driven technology helps companies automate their assessment process, while our experts provide tailored ESG consulting support.

So you can focus on what matters the most: implementing real change across the organization instead of filling out paperwork!

To simplify your EcoVadis journey, we created a five-step infographic: upgrade your ESG strategy and get your copy by clicking here.

The implications of ISO 26000 for companies

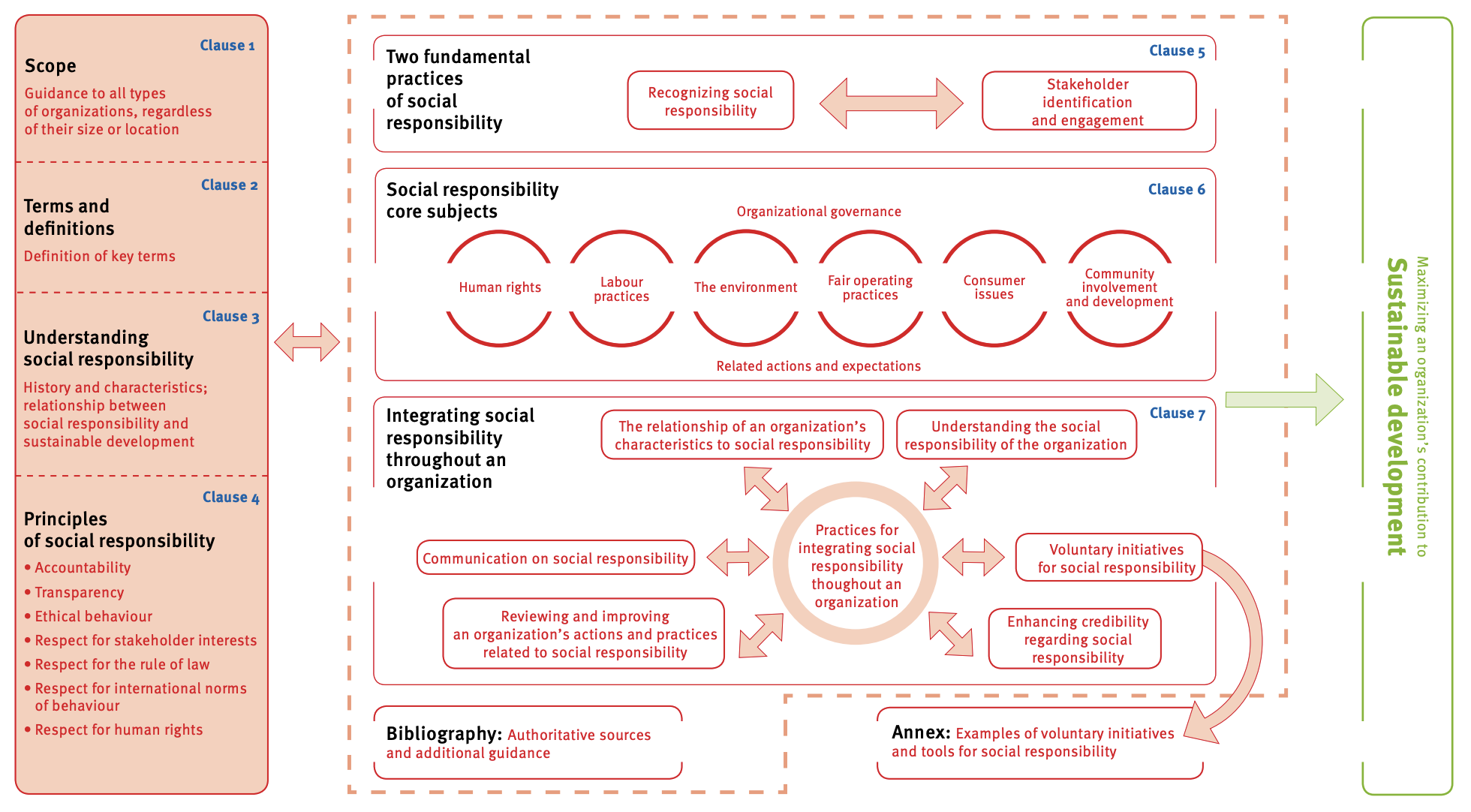

ISO 26000 is an international standard that aims to provide guidance on how companies can be socially responsible. It covers a wide range of issues, from labor rights to environmental responsibility.

The standard is designed for companies that want to implement social responsibility practices in their own operations and within their supply chain.

What is ISO 26000?

The ISO 26000: Guidance on Social Responsibility is a standard for social responsibility published by the International Organization for Standardization (ISO).

It defines social responsibility as “ the responsibility of an organization for the impacts of its decisions and activities on society and the environment through transparent and ethical behavior that:

- Contributes to sustainable development, including the health and welfare of society

- Takes into account the expectations of stakeholders

- Complies with applicable law and is consistent with international norms of behavior

- Is integrated throughout the organization and practiced in its relationships.”

What is ISO 26000 purpose?

The ISO 26000 standard outlines the principles and guidelines of the concept of social responsibility.

The standard aims to help organizations—from companies to NGOs, cooperatives, unions, etc.—operate in a socially responsible way and integrate socially responsible behavior into their organizational culture.

This means that organizations are aware of how their actions and decisions impact people and the environment around them, and act accordingly.

ISO 26000 principles

Social responsibility values

ISO 26000 outlines key values, which are viewed as the roots of socially responsible behavior. As part of their approach to responsibility, companies will make sure to integrate those values within their DNA and in every decision they make.

- Accountability: management takes responsibility for the social and environmental impacts of its operations, supply chain, products/services, and behavior.

- Transparency: the organization shares information about social and environmental performance with all stakeholders.

- Ethical behavior: the organization shows respect for human rights and ensures that its workforce operates in a safe environment. It also ensures that it is not complicit in human rights abuses of others, such as forced or slave labor, by business partners or suppliers.

- Respect for stakeholder interests: the organization shows consideration for the interests and expectations of all stakeholders and manages any negative impacts on their legitimate interests.

- Respect for the rule of law: the organization works within the local and national laws of each country in which it operates.

- Respect for international norms of behavior: the organization operates with integrity and transparency beyond national boundaries.

- Respect for human rights: the organization ensures that it is not complicit in human rights abuses of others, such as forced or slave labor, by business partners or suppliers.

The 7 core subjects

ISO 26000 gives 7 core subjects to work on, related to the organizations’ operations.

The standard insists on the holistic aspect of a social responsibility approach: each of the 7 subjects must be understood as being a constituent element of a coherent whole.

Source: https://www.iso.org

The subjects are then further divided into several subsequent issues, which explain the guidelines that companies are asked to follow. Companies will identify the relevant and priority issues for them.

1/ Organizational governance

Decisions are to be made in consideration of the expectations of society.

Accountability, transparency, ethics, and stakeholders should be factors in the organization’s decision-making process.

2/ Human rights

All humans have the right to fair treatment and the elimination of discrimination, torture, and exploitation.

Issues related:

- Due diligence

- Human rights risk situations

- Avoidance of complicity

- Resolving grievances

- Discrimination and vulnerable groups

- Civil and political rights

- Economic, social, and cultural rights

- Fundamental principles and rights at work

3/ Labor practices

Those working on behalf of the organization are not a commodity. The goal is to prevent unfair competition based on exploitation and abuse.

Issues related:

- Employment and employment relationships

- Conditions of work and social protection

- Social dialogue

- Health and safety at work

- Human development and training in the workplace

4/ The environment

The organization has a responsibility to reduce and eliminate unsustainable volumes and patterns of production and consumption and to ensure that resource consumption per person becomes sustainable.

Issues related:

- Prevention of pollution

- Sustainable resource use

- Climate change mitigation and adaptation

- Protection of the environment, biodiversity, and restoration of natural habitats

5/ Fair operating practices

Building systems of fair competition, preventing corruption, encouraging fair competition, and promoting the reliability of fair business practices help to build sustainable social systems.

Issues related:

- Anti-corruption

- Responsible political involvement

- Fair competition

- Promoting social responsibility in the value chain

- Respect for property rights

6/ Consumer issues

The promotion of fair, sustainable, and equitable economic and social development concerning consumer health, safety, and access is the organization’s responsibility.

Issues related:

- Fair marketing, factual, and unbiased information and fair contractual practices

- Protecting consumers' health and safety

- Sustainable consumption

- Consumer service, support, and complaint and dispute resolution

- Consumer data protection and privacy

- Access to essential services

- Education and awareness

7/ Community involvement and development

The organization should be involved with creating sustainable social structures where increasing levels of education and well-being can exist.

Issues related:

- Community involvement

- Education and culture

- Employment creation and skills development

- Technology development and access

- Wealth and income creation

- Health

- Social investment

Who is ISO 26000 for?

Overview of the different types of organizations using ISO 26000

Organizations in the private, public, and nonprofit sectors, whether large or small, and whether operating in developed or developing countries, use ISO 26000. All of the core subjects of social responsibility are relevant in some way to every organization.

ISO 26000 can be used for example by:

- large multinational corporations

- small and medium-sized enterprises

- the public sector (hospitals, schools or others)

- foundations, charities and NGOs

- extractive industries, such as mining and fossil fuel companies

- service and financial industries (banks, IT, insurance)

- municipal governments

- farmers and agribusiness

- consultancies

Because ISO 26000 offers an operational framework and a practical, pragmatic methodological approach, it can be used by all in any scope: government level, organization level, site level, product/service level and even project/program level.

How does ISO 26000 stand out from other standards and frameworks?

As a voluntary international standard that has emerged from an international consensus, ISO 26000 stands out from others for several reasons:

- It is designed to work in all organizational and cultural contexts – in any country or region

- It is flexible and the user decides how to use it